IRS Forms & Notices Guide

IRS forms decoded. Notices demystified. Whether you're filing for the first time or just got a letter you don't recognize — here's what every form and notice actually means, in plain English.

Section A — Forms You File

15 forms · the documents you fill out and submit to the IRS

U.S. Individual Income Tax Return

The main federal tax return — almost everyone files this. It’s the form that pulls together all your income, deductions, and credits to figure out what you owe (or what you’re getting back).

The 1040 itself is relatively short. Most of the detail lives in numbered schedules that attach to it — Schedule 1 for additional income, Schedule A for itemized deductions, Schedule C for self-employment income, and so on. If you’re a standard W-2 employee with no side income, you may only need the 1040 itself. If your financial life is more complex, expect to attach a few schedules.

Did you know?

The 1040 has gone through major redesigns in recent years. Since 2019 it’s been a shorter “postcard-style” form — most detail now lives in the numbered schedules that attach to it.

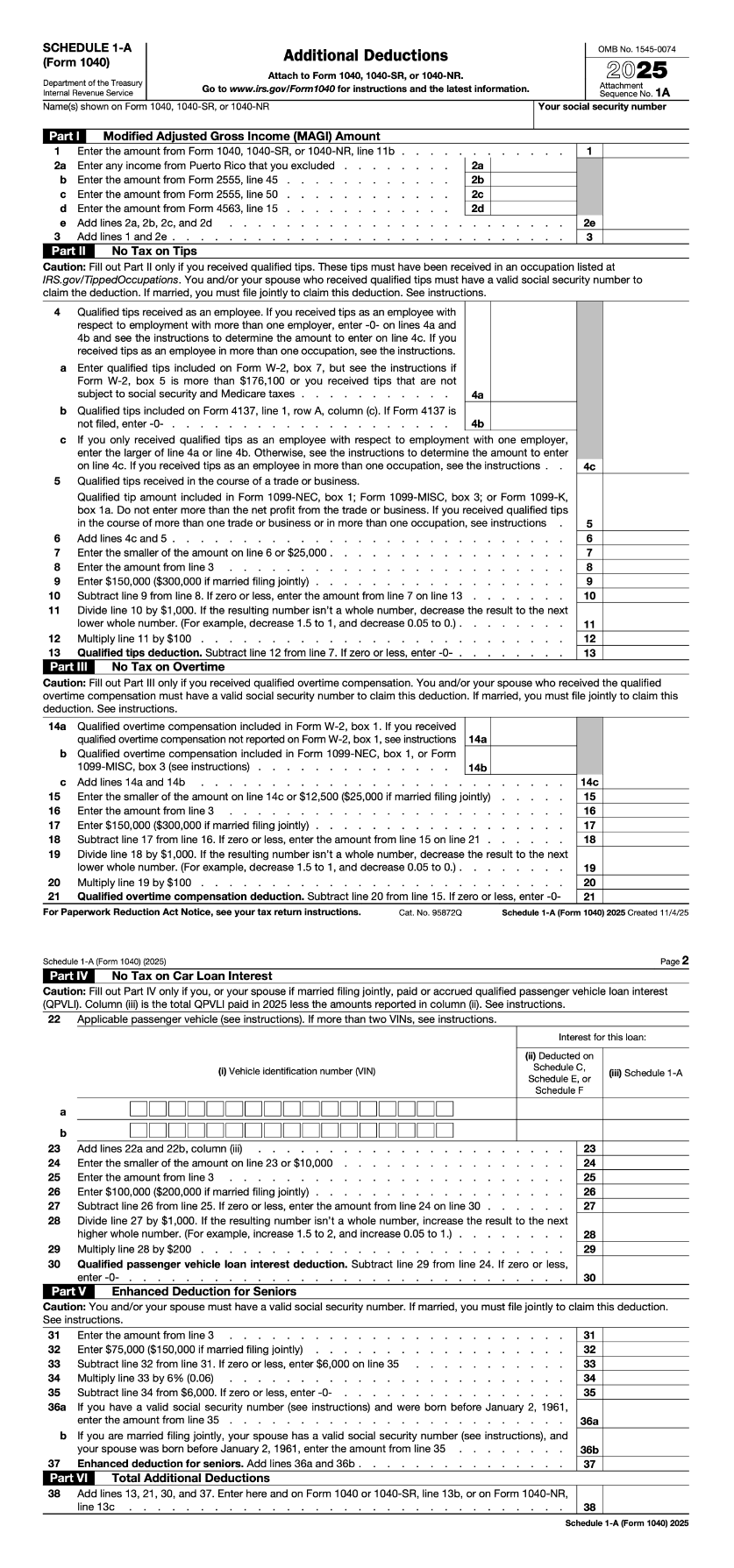

OBBBA Deductions (Tips, OT, Car Loan, Senior)

Brand-new form created by the One Big Beautiful Bill Act for 2025 returns (filed in 2026). Only file it if you’re claiming one of the four OBBBA deductions: the tips deduction, overtime deduction, car loan interest deduction, or the senior bonus deduction. If none of those apply, skip it.

Schedule 1-A lives alongside the regular numbered schedules but exists specifically for these four new deductions. Each deduction has its own income cap and eligibility rules — not every tip worker or senior automatically qualifies.

-

1

Part I — MAGI

Modified Adjusted Gross Income. This is your starting point — every deduction on this form phases out based on your MAGI, so this number determines what you actually qualify for.

-

2

Part II — No Tax on Tips

Deduct up to $25,000 in qualified tips from your taxable income. Only tip workers in IRS-listed occupations qualify. Phaseout starts at $150,000 MAGI ($300,000 joint).

-

3

Part III — No Tax on Overtime

Deduct the premium portion of overtime pay — the "half" of time-and-a-half, not the base. Max $12,500 single / $25,000 joint. Same MAGI phaseout as tips.

-

4

Part IV — Car Loan Interest

Deduct up to $10,000 in interest on a new vehicle loan. New cars only (no used), US-assembled, personal use, loan originated in 2025. Leases don't qualify.

-

5

Part V — Senior Deduction

Extra $6,000 deduction for filers age 65+. Stacks on top of the standard senior additional deduction. Phases out starting at $75,000 MAGI ($150,000 joint).

-

6

Part VI — Total

Sum of all four deductions from the parts above. This total flows to Form 1040, line 13b — reducing your taxable income but not your AGI.

Tax tip

These are “below the line” deductions — they reduce your taxable income but don’t affect your AGI. That means claiming them won’t hurt your eligibility for AGI-based credits like the Child Tax Credit.

Employee's Withholding Certificate

The form you give your employer to tell them how much federal income tax to withhold from your paycheck. Filling it out wrong is one of the most common reasons people owe a surprise bill at tax time — or get a giant refund (which just means you overpaid all year and loaned the government money interest-free).

You fill out the W-4 once when you start a job, and that’s usually the last time anyone thinks about it. But life changes — and so should your W-4.

Heads up

You should re-file your W-4 any time your life changes — marriage, divorce, a new baby, a second job, or a major income change. The IRS Withholding Estimator can help you figure out the right settings.

Income Reporting Forms

The 1099 is the family of forms that reports income you received outside of a regular paycheck. There are over a dozen variants — here are the four most common ones most people will encounter.

You don’t fill these out yourself. Whoever paid you (a client, a platform, a brokerage) sends you one, and sends a copy to the IRS. Your job is to report the income on your return and make sure what you report matches what the IRS already has.

Nonemployee Compensation

Freelance & contractor income. If you got one, you're responsible for self-employment tax on those earnings.

Payment Card and Third Party Network Transactions

Payment apps & platforms (Venmo, PayPal, Etsy, eBay). Under OBBBA, the threshold returned to $20,000 AND 200 transactions.

Miscellaneous Information

Rent, royalties, prizes, awards. Not the same as 1099-NEC — different box numbers, different rules, different tax treatment.

Distributions from Pensions, Annuities, Retirement Plans

Retirement account distributions. Distribution codes matter — early withdrawal, rollover, and Roth conversion all get treated differently.

Did you know?

Getting a 1099 doesn’t automatically mean you owe taxes on the full amount. Personal Venmo reimbursements, for example, are not taxable income — but the platform may still issue the form if it crosses the threshold. Always check whether the income is actually taxable before you panic.

Profit or Loss From Business

If you made money as a sole proprietor — freelancing, consulting, driving for Uber, selling on Etsy, running a one-person business — Schedule C is where you report it. You list your gross income at the top, subtract your legitimate business expenses, and the net number flows to your 1040.

Schedule C is where most small business deductions happen: home office, mileage, software subscriptions, professional services, supplies. Keep receipts for everything — if you get audited, “I just remember it was about $3,000” isn’t going to cut it.

Tax tip

Net profit on Schedule C triggers self-employment tax (15.3% on top of income tax). Half of the SE tax is deductible above the line, which softens the blow — but new freelancers are often blindsided by how much they owe. Set aside roughly 25-30% of your net profit for taxes as you go.

Self-Employment Tax

If you netted $400 or more in self-employment income, you owe Social Security and Medicare tax on it — and you file Schedule SE to calculate it. W-2 employees split these taxes with their employer (7.65% each). Self-employed people pay both halves themselves, totaling 15.3%.

Schedule SE is short and mostly mechanical: plug in your Schedule C net profit, apply the 92.35% factor, multiply by 15.3% (up to the Social Security wage base), and you’ve got your SE tax.

Did you know?

You can deduct the employer-equivalent half of your SE tax on Schedule 1 as an adjustment to income. It doesn’t eliminate the tax — but it does lower your AGI, which can help with other credits and deductions.

Itemized Deductions

Schedule A is where you itemize deductions instead of taking the standard deduction. The main categories are state and local taxes (SALT), mortgage interest, charitable contributions, and medical expenses above 7.5% of AGI.

Most people don’t itemize anymore. The 2017 tax law roughly doubled the standard deduction, and OBBBA pushed it higher still — which means itemizing only beats the standard deduction for homeowners in expensive areas, high earners with big charitable giving, and a handful of other cases.

Tax tip

Compare both ways before filing. Tax software does this automatically, but it’s worth understanding: you take whichever number is bigger. You can’t mix and match — it’s all-or-nothing.

Wage and Tax Statement

Your employer’s record of what they paid you and what they withheld. You get one from every employer you worked for during the year, usually by late January. The numbers on the W-2 go directly onto your 1040 — Box 1 is wages, Box 2 is federal tax already withheld, Box 12 is where things like 401(k) contributions show up with letter codes.

You don’t fill out a W-2. Your employer does. Your job is to make sure the numbers match what your pay stubs showed all year, and to include it with your return.

Heads up

If you haven’t gotten a W-2 from a former employer by mid-February, contact them first. If that doesn’t work, the IRS can help — but you may need to file using Form 4852 (a substitute W-2) if the deadline is approaching.

Trump Account Election(s)

Brand-new form created under OBBBA. Parents and other authorized individuals use it to open a Trump Account — a new type of tax-advantaged savings account for children under 18 — and to claim the one-time $1,000 federal pilot contribution for kids born 2025–2028.

You can file Form 4547 with your 2025 return (due April 15, 2026) or by itself at any time. Contributions to Trump Accounts can’t begin until July 4, 2026, but you need the election filed before then to have an account ready.

Did you know?

Only one authorized individual can open a Trump Account per child, and there’s a priority order — legal guardian first, then parent, then adult sibling, then grandparent. If your child has a guardian, neither parent can do it unilaterally.

Application for Automatic Extension of Time to File

If you can’t file your tax return by April 15, submit Form 4868 and you automatically get an extra six months — pushing your filing deadline to October 15. No explanation required, no approval needed. The IRS grants the extension automatically.

The catch everyone misses: this is an extension to file, not an extension to pay. If you owe taxes, you still need to estimate what you owe and pay it by April 15. Otherwise, interest and late-payment penalties start accruing on the unpaid balance.

Heads up

Filing a 4868 is not an extension of your payment deadline. Pay your best estimate by April 15 even if you haven’t finished your return. You can pay electronically through IRS Direct Pay and skip filing the form entirely — making a payment with the “extension” reason code automatically files the extension for you.

Interest Income

If your bank, brokerage, or credit union paid you more than $10 in interest during the year, they send you a 1099-INT. The number in Box 1 gets reported as taxable income on your 1040 (usually on Schedule B if you have multiple accounts or more than $1,500 in interest total).

This includes interest from regular savings accounts, CDs, money market accounts, corporate bonds, and Treasury bonds (though Treasury interest is federal-taxable only — your state can’t touch it).

Tax tip

Interest income is taxed at your ordinary income tax rate, not the lower capital gains rate. If you’re in a high bracket, municipal bonds (which are federally tax-exempt) can make more sense than taxable bonds even at lower yields.

Dividends and Distributions

If you own dividend-paying stocks, mutual funds, or ETFs, you’ll get a 1099-DIV reporting what they paid you. The critical split is between Box 1a (ordinary dividends, taxed at your regular income rate) and Box 1b (qualified dividends, taxed at the lower long-term capital gains rate).

Most dividends from U.S. stocks you’ve held long enough are qualified. Dividends from REITs and some foreign sources usually aren’t. Your brokerage sorts this out for you on the form.

Did you know?

Qualified dividend tax rates are 0%, 15%, or 20% depending on your taxable income — and the 0% bracket is broader than most people realize. A married couple with under roughly $96,000 in taxable income pays nothing on qualified dividends. That’s not a typo.

Estimated Tax for Individuals

If you have income that doesn’t have tax withheld from it — self-employment income, big investment gains, rental income, large IRA withdrawals — you generally need to pay estimated taxes four times a year instead of waiting until April. Form 1040-ES is both the worksheet that helps you figure out how much to pay and the voucher you send with your payment.

The quarterly deadlines are April 15, June 15, September 15, and January 15 of the following year. Miss them or underpay and you owe an underpayment penalty — even if you pay everything by April 15 the next year.

Tax tip

The “safe harbor” rule: you generally avoid underpayment penalties if you pay either 90% of this year’s total tax liability or 100% of last year’s (110% if your AGI was over $150,000). Hitting the prior-year safe harbor is easier because you already know the number.

Digital Asset Proceeds from Broker Transactions

New form that crypto brokers and platforms started issuing for the 2025 tax year. If you bought, sold, swapped, or otherwise transacted in digital assets through a broker, you’ll get a 1099-DA showing the gross proceeds.

Heads up: the 1099-DA may not include your cost basis for every transaction. If your broker didn’t track what you originally paid, you need to use your own records to calculate gain or loss. Keep every trade confirmation — this is not the year to wing it on crypto reporting.

Heads up

The digital asset question on Form 1040 must be answered yes or no — you can’t leave it blank, even if you only bought crypto and didn’t sell anything. If you sold, swapped, or were paid in digital assets, you need to report gain or loss on Form 8949 and carry the totals to Schedule D.

Change of Address

If you moved since filing your last return, use Form 8822 to tell the IRS your new address. It’s one page, takes two minutes, and prevents a surprising amount of tax-related trouble.

Why does this matter? Because the IRS sends all notices and refund checks to the last address on file. If a CP14 balance-due notice goes to your old place and sits unopened for 60 days, you can end up in collections on a debt you never knew existed. Most people who get to CP504 got there because earlier notices were sent somewhere they no longer lived.

Tax tip

You can also update your address just by putting the new one on your next tax return. But if you moved mid-year and are expecting anything from the IRS before then (a refund check, a notice, an identity verification letter), file Form 8822 now.

Section B — Notices & Letters the IRS Sends You

8 notices · what that envelope in your mailbox actually means

Balance Due — First Notice

This is the first letter the IRS sends when you owe taxes. It includes the amount due, plus any penalties and interest that have already accrued. It’s not an audit — it’s a bill.

CP14 is generated automatically after the IRS processes your return and sees a balance due. Receiving one doesn’t mean you did anything wrong — you filed correctly, but the payment didn’t come through or wasn’t enough.

WHAT TO DO

You have 21 days from the notice date to respond. You have three main options: pay in full, set up a payment plan, or dispute the amount if you believe there’s an error.

Don’t ignore it. Ignoring CP14 is what leads to CP503, CP504, and eventual collection action. If you can’t pay the full amount, a payment plan is easy to set up online and stops the escalation.

Intent to Levy — Final Notice

This is the IRS telling you they intend to seize your assets — your state tax refund first, then potentially your bank accounts, wages, or other property. This is the last stop before collection action begins.

You only get here after ignoring earlier notices. Most people who reach CP504 did so because earlier notices (CP14, CP501, CP503) went unanswered — sometimes because they were sent to an old address.

WHAT TO DO

Do not wait. You have 30 days to respond before the IRS can act on the levy. Options include paying in full, requesting a payment plan, filing an Offer in Compromise if you genuinely can’t afford the debt, or requesting a Collection Due Process hearing to dispute it.

This is the point where professional help is strongly recommended. A tax professional or enrolled agent can often negotiate better terms than you can on your own, and the 30-day window gives you time to find one.

Tax tip

Keep your address current with the IRS. You can update it by filing Form 8822 or by including your new address on your next return. The IRS mails all notices to the last address on file — they won’t call or email first.

Underreporter Notice — Proposed Changes

The IRS found a mismatch between what you reported on your return and what was reported to them by employers, banks, or platforms — usually a 1099 you forgot about or a brokerage statement you didn’t include. This is not an audit. It’s a proposed adjustment.

The CP2000 will show you line by line what the IRS thinks should change and how much that changes your tax. It’s essentially the IRS saying “here’s what we would have calculated if you’d included this income — do you agree?”

WHAT TO DO

You can agree, partially agree, or dispute a CP2000. You have 30 days to respond (60 if you live outside the U.S.). If the IRS is wrong — for example, a 1099 was issued in error, or the income was already included somewhere else on your return — respond with documentation explaining why.

If the IRS is right, the fastest resolution is to agree, sign the response form, and pay (or arrange to pay) the additional amount. Disputing a correct CP2000 just delays the inevitable and lets interest accrue.

Did you know?

CP2000 is one of the most common IRS letters — the IRS sends millions every year, mostly for routine mismatches. Getting one is not a sign you’re being audited or targeted. It’s a sign the automated matching system flagged something worth a second look.

Math Error — Balance Due

The IRS reviewed your return, found what they believe is a math or calculation error, corrected it — and the correction means you owe more money than you calculated. The notice shows what they changed and the new balance due.

Despite the name, “math error” covers more than arithmetic. It includes things like claiming a credit you don’t qualify for, dependency issues, or entries that don’t match what the IRS has on file.

WHAT TO DO

Read the notice carefully. If the correction is legitimate and you owe the new amount, pay it by the due date to avoid additional penalties and interest.

If you disagree, you have 60 days to request abatement. Respond in writing with documentation supporting your original numbers. If the IRS agrees, the correction is reversed. If you miss the 60-day window, you lose the right to challenge the math-error adjustment — you’d then have to pay and file a claim for refund, which is a much longer process.

Math Error — Refund Change

Similar to CP11, but this one comes with good news (usually). The IRS reviewed your return, corrected what they believe was a math or calculation error, and the result is either a refund you didn’t expect or a bigger refund than you filed for.

Sometimes it’s a smaller refund than you expected — they reduced what you claimed — but the account still has money coming to you. The notice explains exactly what they changed.

WHAT TO DO

If you agree with the change, there’s nothing to do — the refund will arrive by mail or direct deposit in 4–6 weeks.

If you disagree (for example, you think your original refund was correct and they reduced it unfairly), you have 60 days to contest it. Respond in writing with documentation. After 60 days, challenging the adjustment gets much harder.

Did you know?

CP11 and CP12 come from the same IRS process — the automatic math verification system. The only difference is which direction the correction went. Both require a 60-day response window if you disagree.

Audit Report — 30-Day Letter

You get Letter 525 after the IRS finishes auditing your return (by correspondence — if your audit was in person, you’d get Letter 915 instead). Attached is Form 4549, the examination report showing proposed adjustments to your tax.

This is the IRS’s final proposal after the audit. You have 30 days to agree, disagree, or ask for more time.

WHAT TO DO

If you agree with every proposed change, sign and return the form. You’ll get a bill for any additional tax, and the audit is closed.

If you disagree, respond within 30 days with a written statement explaining why and supporting documentation. You can also request a conference with the examiner’s manager, or appeal to the IRS Independent Office of Appeals.

If you miss the 30-day window, the IRS can issue a Notice of Deficiency — giving you 90 days to petition the Tax Court. After that, the proposed changes become final and collectible.

Initial Audit Notification

Letter 566 is the starting gun of a correspondence audit. The IRS selected your return for examination and wants documentation to support specific items — usually a credit you claimed (like EITC or education credits), a deduction, or reported income.

The letter lists exactly what’s under review and what documents you need to provide. You’re not in trouble yet — you’re being asked to prove what you already reported.

WHAT TO DO

Gather the requested documents and respond by the date on the letter. Most correspondence audits are resolved in your favor if you can substantiate what you claimed. Keep copies of everything you send, and use certified mail or the IRS’s Document Upload Tool for proof of submission.

If you can’t find the documentation, don’t give up — bank statements, third-party records, and written explanations can sometimes substitute for missing receipts. If the audit gets complicated, consider hiring a tax professional or contacting a Low Income Taxpayer Clinic for free help.

Tax tip

Respond even if you can’t fully prove every item. A partial response is almost always better than no response. If you ignore Letter 566 entirely, the IRS disallows everything in question and issues Letter 525 (the 30-day letter) with the full proposed adjustment.

Notice of Federal Tax Lien

Form 668(Y) is the IRS filing a public notice that you owe them money. A federal tax lien is the government’s legal claim against your property — real estate, vehicles, financial accounts, business assets, and anything you acquire while the lien is in effect.

The lien itself attaches automatically when you don’t pay an assessed tax debt. Form 668(Y) is the IRS making that lien public, which is what causes the real-world damage: creditors can see it, it affects your ability to borrow, and it attaches to property you try to sell.

WHAT TO DO

Pay the tax in full if you can — the IRS releases the lien within 30 days of full payment. If you can’t pay in full, consider a Direct Debit Installment Agreement: once you’ve made three consecutive payments under a DDIA (and owe less than $25,000), you can apply to have the lien withdrawn.

You have 30 days from the filing to request a Collection Due Process hearing through the Office of Appeals. This is one of the few chances to formally dispute the lien before it becomes a long-term fixture on your record.

Did you know?

Federal tax liens no longer appear on consumer credit reports (this changed in 2018), but they’re still public records. Lenders, landlords, and employers who dig into public records — which many do — can find them. Getting a lien withdrawn after payment is worth the paperwork.

Common questions

It might be. The IRS almost never calls or emails first — they mail paper notices. If you got an email, text, or phone call claiming to be the IRS and demanding immediate payment, it’s very likely a scam. Verify any notice by looking up the notice code (like CP14 or CP2000) on IRS.gov directly. Never click links in unsolicited tax-related messages.

The IRS generally has three years from the date you filed to audit a return. That window extends to six years if they suspect you underreported income by more than 25%, and is unlimited if they suspect fraud or if you never filed at all. Keep your own records at least seven years to be safe.

You have options. The IRS offers short-term payment plans (up to 180 days), long-term installment agreements, and in rare cases an Offer in Compromise that settles the debt for less than you owe. The worst move is ignoring the notices — penalties and interest keep accruing, and eventually the IRS starts collection action. File on time even if you can’t pay, then set up a plan.

Digital copies are fine as long as they’re legible and complete. Keep tax returns, W-2s, 1099s, and proof of deductions for at least three years (seven to be safe). For anything related to property you still own — a house, investments — keep the records as long as you own the asset plus three years after you sell.

Contact the employer or payer first. If you don’t have it by mid-February, call the IRS at 800-829-1040 and they’ll send the employer a reminder. If the deadline is approaching and you still don’t have it, file with Form 4852 as a substitute — but only as a last resort, since filing without the actual form can delay your refund if the numbers don’t match.

ON THIS PAGE

Back to topGet this explained in your inbox

We break down IRS forms and notices like this every week — no jargon, no snooze-factor. Free forever.

Free as a meme, easy to bail anytime.